Industry Insights

In 2023, the aviation industry will likely see steady growth and favorable relief for some insurance buyers. While rates have increased over the last five years, the broader aviation market seems to remain stable. Factors affecting aviation insurance include pilot experience, loss history, and economic uncertainty — all of which contribute to risk-specific characteristics and determine client outcome.

While growth is on the docket in 2023, worldwide tensions — particularly related to Russia’s confiscation of more than 400 airplanes and parts leased from Western companies — continue to be a point of contention. The final sum (expected to exceed $10 billion) will depend on whether losses are “All Risks,” “Hull War,” a combination of the two, or if they are losses insurers can successfully deny. If denied, this will have significant ramifications on future pricing of premiums.

Another factor affecting the aviation industry is rising oil prices. Fuel is one of the major costs of operating an aircraft. Spikes in fuel prices can have a significant impact on profitability and can be difficult to manage.

Increased demand for air travel combined with a shortage of qualified pilots and maintenance technicians is also of concern. All sectors of aviation are struggling to hire and retain qualified pilots and maintenance personnel. With the high costs and shortage of simulator training facilities and instructors, the bottleneck continues to be problematic. For employees, competitive salaries and benefits will be challenges moving forward.

In addition to training costs, pilot training standards continue to be more stringent with underwriters requiring annual full-motion, simulator-based training. Training facilities are running 6-12 months behind schedule due to lack of qualified trainers, and classes are maxed at full capacity.

Single pilot (SP) operations for more complex aircraft and jets are slowly disappearing, especially for Part 135 commercial operations. Most insurers are no longer offering this coverage, and the few that offered it in 2022 averaged costs two-thirds higher than Dual-Crew (DC) operations. For consideration, some markets may offer SP for U.S. travel and DC outside the U.S.

Due to the nature of aviation exposures and catastrophic loss and because there are too few aircraft risks for the “law of large numbers” to predict loss, aviation insurers rely on their own judgments and reinsurance costs when determining hazards. One such “hazard” is older model aircraft. During annual and pre-buy inspections, maintenance personnel often find corrosion, which in some cases is unrepairable.

Adding to these higher costs are repair or replacement parts. As the aircraft ages, insurers are cautious because of the high likelihood of a total loss. With inflation and rising interest rates driving up fuel costs, material costs, claims costs, and labor rates, it is likely the aviation industry will be challenged. However, if travel demand remains steady, the industry will likely weather the turbulence moving forward.

Recommendations

Aviation is unique and complex, so partnering with an aviation insurance specialist is a great strategy for risk management. Pertinent information will need to be shared to ensure accuracy of coverage, but there are also actions the owner/operator can take to mitigate risks.

- Assess risk exposures in practical terms and focus on identifying, addressing, and managing the factors outside your control that can lead to an occurrence.

- Choose a partner broker who understands the industry and specializes in “all risk” aviation. It is important that a risk be seen in its best light when presented to underwriters, and that specialized brokers with underwriting relationships articulate the risk clearly and concisely to navigate the market successfully.

- Ensure you meet all underwriting guidelines and pilot training requirements.

- For older pilots, seek markets who support high-qualified pilots who obtain first class medicals along with additional medical testing (i.e., annual stress test).

"Factors affecting aviation insurance include pilot experience, loss history, and economic uncertainty — all of which contribute to risk-specific characteristics and determine client outcome."

Industry Insights

This past year saw less investment funneled into the cannabis space compared to previous years; however, we continued to see overall industry growth. As more states legalize cannabis, either medically or for recreational use, there is corresponding growth in cannabis ancillary businesses.

This past year saw less investment funneled into the cannabis space compared to previous years; however, we continued to see overall industry growth. As more states legalize cannabis, either medically or for recreational use, there is corresponding growth in cannabis ancillary businesses.

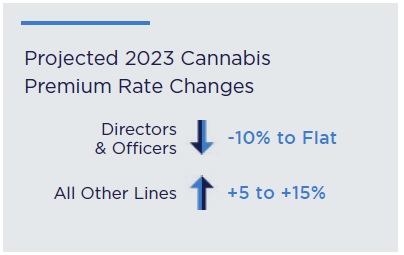

Historically, one of cannabis operators’ biggest spends is D&O (directors and officers) insurance. Due to our litigious environment, we often see a higher cost associated with D&O, lower limits, and higher retentions. As we move into a softer D&O market, we have already seen much more favorable pricing for the cannabis space.

The biggest challenge this year stems from the expected downturn in the economy, as labor shortages and supply chain issues continue. The cannabis industry should be aware of emerging issues and kept abreast of insurance market dynamics as we see more states and insurers join the space.

"As we move into a softer D&O market, we have already seen much more favorable pricing for the cannabis space."

Recommendations

With an ever-changing landscape, those in the cannabis industry can take several measures to help prepare for shifts and minimize impact. In addition to being proactive, organizations should:

- Establish full trust and transparency to ensure correct coverages are in place and systems can handle incoming claims.

- Prepare a marketing strategy early in the process and create a quality submission highlighting “good risk” qualities.

- Partner with the right specialist brokers, especially for D&O insurance. Having someone who understands the cannabis space and has the right connections and direct appointments is crucial to secure the best options possible.

- Invest in product liability/product recall coverage as well as E&O insurance.

- Have a robust employee benefits package in place. This can help recruit and retain talent, an issue with which the industry is currently struggling.

- Conduct broker-client meetings throughout the year in order to ensure that important aspects, like fleet/driver safety, workers’ compensation claims, D&O insurance, and others are discussed. This is critical for underwriting and can help ease board member stress.

Industry Insights

In 2023, colleges and universities are facing multiple business, talent, and technology issues, all contributing to rising risk factors and the cost of insurance.

In 2023, colleges and universities are facing multiple business, talent, and technology issues, all contributing to rising risk factors and the cost of insurance.

According to the National Association of College and University Business Officers (NACUBO), the top business challenges include:

- Supporting and maintaining the workforce. Colleges/universities are experiencing the same labor issues facing many US industries such as talent shortages, and the need for competitive wages and benefits to attract and retain personnel.

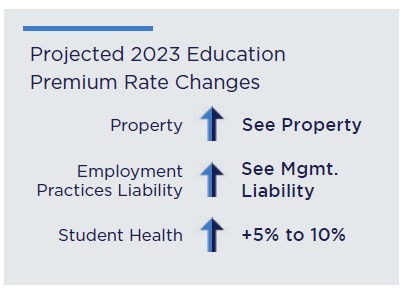

- Meeting students’ evolving needs. Educational institutions are dependent upon tuition revenue. In recent years, they have seen falling enrollment and higher dropout rates. Stress is a major contributor to dropout rates. The need for student mental health and wellness services was recently ranked as a top issue in the Risk Strategies 2022 Second Annual Student Health Plan Benchmarking Survey.

- Securing a modern technology infrastructure. Inflation, rising costs for materials and labor, supply chain issues, as well as weather-related catastrophic events are all contributing to escalating property risks. Cybersecurity risks continue to grow, as colleges and universities have been primary targets of cyber criminals.

Recommendations

Robust risk management practices are more important than ever to address the evolving risks. A specialty broker who has deep experience in the education sector can help you understand your risk profile and navigate the renewal process.

- For property & casualty, understand your CAT exposures through modeling, up-to-date property valuations, and document loss prevention improvements. Meet with underwriters and invite them to your campus for a tour.

- Do a detailed review of general and educators’ liability programs, as well as cyber, D&O, and property coverage. Ensure you have adequate coverage for your risks.

- Consider tuition insurance as an “opt out” rather than a voluntary program. This can decrease the potential loss of enrollment and support retention. For students who withdraw for a period, and their families, this is valuable protection to not lose their tuition contribution, making it more likely the students will return to campus.

- For student health plans, consider higher deductibles and/or higher utilization of telehealth, as costs are lower and more convenient than in-person therapy.

Industry Insights

The entertainment industry will see continued supply and demand driving TV and film content creation.

The entertainment industry will see continued supply and demand driving TV and film content creation.

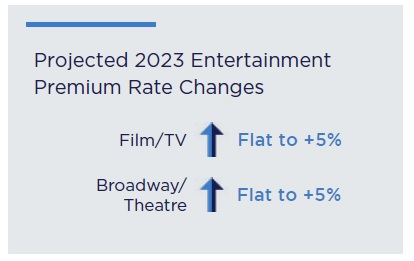

Given the substantial rate increases that occurred in 2020 and 2021, the entertainment industry no longer appears to be in a hard market, as rates have stabilized for the most part.

However, COVID-19 continues to impact production with the need for maintaining on-set safety protocols and continued calls for better COVID-19-related workplace environments. In turn, there is still a search for mass-market COVID-19/Communicable Disease coverage solutions.

Events are growing in number as many COVID-19 restrictions are being lifted for live performance attendance. Nevertheless, the live theatrical and venue space continues to experience a hardening pricing market.

The live performance space is facing a difficult time as markets are limited. In turn, venues will see coverages and previously offered limits scaled back from 2022 levels. There is some new capacity attempting to come into the marketplace offering somewhat more competitive rates on certain risks. If the new capacity is successful in gaining traction with businesses, rate increases could potentially level off or come down slightly in 2023.

The venue marketplace has not faced the same challenges, but depending on the type and size of events being held, there are issues with markets being unwilling to offer the same level of coverage they have offered in the past. Additionally, they are looking for some rate increases depending on the type of event, size, and the loss experience of the individual client.

Coverage Considerations

Specialty coverage (production, event cancellation, etc.) rates for film, TV, and contingency businesses appear to be flattening. However, key coverages such as cyber liability, as well as auto, general, and excess liability remain difficult.

After suffering large losses, contingency insurance rates are also increasing, most notably for performance disruption, non-appearance, and abandonment coverage.

After suffering large losses, contingency insurance rates are also increasing, most notably for performance disruption, non-appearance, and abandonment coverage.

While underwriting in the entertainment space — including TV, film, performing arts, and events — has become more disciplined and stringent following the COVID-19 pandemic, it does now appear as though the market is softening slightly and insurance carriers are becoming more prepared to negotiate risk rather than flatly reject as in the past.

There is continued hardening in the marketplace for large publicly attended events, given large losses in the past few years, as well as concern in the marketplace around inflation, social inflation, and the effects of a recession.

Recommendations

Every year presents new insurance and risk management considerations for the entertainment industry. We advise the following:

- Meet with a specialist at least annually to discuss trends, evaluate risks, review coverages, and explore alternatives for financing risk.

- Underwriters are asking for more information in 2023. Documenting continuous commitment to risk management will help secure the best available rates and terms.

- Begin planning for new coverages and renewals early. Build in ample time for review and discussions with carriers.

- Request contract reviews from a specialty insurance broker, not just your attorney. Risk management and insurance issues may be lurking in the fine print.

- For TV productions, movies, television advertising, and live theater, ask a specialty broker for script reviews to identify potential risk and insurance concerns.

Industry Insights

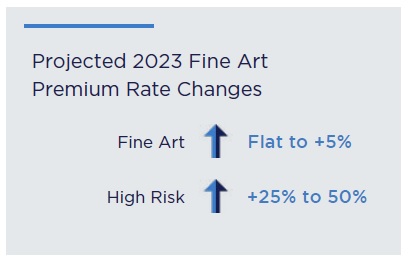

The fine art market remains robust, as we saw a 47% increase in public sales and a 18% increase in the dealer market in 2022. Postwar and contemporary art continue to have the strongest values. The top end of fine art is expected to remain resilient to economic contractions in 2023. The rapid appreciation of art values drives an ever-expanding rating basis in this segment.

The fine art market remains robust, as we saw a 47% increase in public sales and a 18% increase in the dealer market in 2022. Postwar and contemporary art continue to have the strongest values. The top end of fine art is expected to remain resilient to economic contractions in 2023. The rapid appreciation of art values drives an ever-expanding rating basis in this segment.

Those located in catastrophe-prone (CAT) locations will experience significant insurance coverage challenges. Risks with few to no mitigation techniques or with a difficult claim history will find it hard to get reasonable coverage. Underwriters are also evaluating emerging climate change-associated risks. Coverage in CAT areas is exacerbated by the continued, rapid increase in art values, especially in California and Florida, where earthquake and windstorm aggregations are already nearing a tipping point.

Specific concerns for the fine art industry in 2023 include:

- Fine art warehouse facilities face aggregation issues. Skyrocketing art values are impacting newer locales such as Aspen, where the ultra-wealthy house some of their large collections.

- Some European art fairs have become more rigorous with their exhibitor liability requirements. Liability limit requirements are as high as $10 million, requiring dealers to increase their umbrella limits or purchase coverage from the fair.

- Museums are beginning to seek specialist advice regarding how climate change can affect them. It is essential for museums to prepare for the future and ensure their collection and incoming loans are protected. In addition, museums should consider how climate change could affect facilities to which they agree to outgoing loans.

- NFTs are still a presence in the art world. While it is virtually impossible to insure an NFT, it is possible to insure the key codes if stored with a third party. The fluctuating value of crypto is not insurable in the fine art market, so a set value is required for insuring anything related to NFTs.

Coverage Considerations

Underwriters are requiring more information than ever to issue quotes. They are tightening up requirements after paying significant claims on large private collections and express carrier claims.

Appraisals for higher-valued items are a coverage requirement, as are full shipping details.

Appraisals for higher-valued items are a coverage requirement, as are full shipping details.

Signs point to significant rate increases in natural catastrophe zones, with little to no increase to noncatastrophic risks. Despite the increasing value of art, the protections around art risks have shielded the insurance market from large claims, leading to a slight market “softening” for non-catastrophic risks in 2023.

Due to worker shortages, some of the first- and last-mile fine art shippers’ quality has waned. Underwriters want specific shipping companies and details surrounding the works and travel arrangements. Skyrocketing air freight costs and environmental impact concerns have some seeking alternative shipping methods via ocean freight. Almost all forms of art are at greater risk of loss or damage when shipped by ocean freight due to a lack of climate control and transport delays caused by port congestion.

Recommendations

- Stay on top of art values. It is critical to understand the sum of values at each insured location. Most collections need to be reappraised every 3-5 years. To have the broadest collection coverage, underwriters will ask insureds to commit to this schedule.

- Be prepared with granular underwriting information including fire and burglary protection, as well as retrofitting, relative to all locations.

- Make sure you are protected from catastrophic risk and consider reallocating some highervalued works to non-catastrophic locations or bringing in a consultant who can advise on loss mitigation practices. Disaster response and evacuation plans will be critical for those in catastrophe zones.

- Gather all relevant shipping details, drill down on first- and last-mile shipment details, and be prepared to relay these details to a broker/insurance company.

- Give a broker plenty of notice prior to switching or moving into a new fine art warehouse to get the best possible coverage for your warehouse of choice.

- Consider political violence/full terrorism coverage when lending or consigning artworks to or attending fairs in countries experiencing political unrest.

Property & Casualty

Industry Insights

For many healthcare organizations, 2022 was a financially difficult year due to the labor shortage, unpredictable volumes, and higher cost of services. These issues will likely continue in 2023, and healthcare organizations will have to make decisions about services provided to remain viable in the future.

For many healthcare organizations, 2022 was a financially difficult year due to the labor shortage, unpredictable volumes, and higher cost of services. These issues will likely continue in 2023, and healthcare organizations will have to make decisions about services provided to remain viable in the future.

The effect of the healthcare labor shortage is being closely monitored by the markets as it is unclear how it will impact the provision of care, financial viability of organizations, and future claim activity. Additionally, inflation has been affecting all facets of life, and healthcare is in no way immune to this.

Healthcare consolidation continues at a steady rate. For the first time, healthcare mergers and acquisitions activities exceeded $200 billion in 2021. We see private practices merging or being acquired by larger healthcare organizations or private equity investors. Independent and regional hospitals are getting acquired by larger healthcare systems. The impact of consolidation on quality of care and overall costs for consumers continues to be a concern.

Coverage Considerations

Professional Liability

The severity of professional liability claims continues to increase due to social inflation and the rise of nuclear verdicts. Carriers continue to be concerned about the uncertainty surrounding the court systems and COVID-19 claims as well as the future impact inflation has on medical expenses.

Pending bills and changes to laws in certain jurisdictions (the venue shopping rule in PA, MICRA in CA, and the Dobbs Supreme Court Decision) are being closely monitored to determine if and how they may impact healthcare providers and the insurance marketplace.

Professional liability (except physician medical malpractice) rate increases are beginning to taper off, but the increased severity of claims and certain venues continue to impact the availability of excess capacity.

The physician medical malpractice market continues to see hard market conditions throughout the country. Rate increases up to 15% are expected to continue in 2023. Admitted markets are taking more conservative stances and are non-renewing poor performing risks. As a result, the excess and surplus lines market is being accessed where rates are typically higher, and terms are more restrictive.

Property

Underwriters are focused on adequacy of values and are closely reviewing capacity, terms/conditions, and deductibles. Carriers are looking at reducing CAT peril limits due to recent severe weather events and are proposing increased deductibles.

Auto

Healthcare auto continues to be a challenging line of business, particularly when clients have emergency vehicles, or a significant non-owned exposure exists. Many underwriters will not offer auto without a supporting line of business which is why auto is often placed with property with the same carrier.

Cyber

Cyberattacks and coverage will continue to be a major concern for the healthcare industry, which necessitates a continued focus on thorough underwriting and cyber hygiene. Underwriting questions continue to evolve, based on developing issues or cyber related claims. Premium increases, retention increases, and coverage restrictions are expected for 2023 but not at the same level as the past two years. Coverage limitations are added if proper IT cyber controls, especially multi-factor authentication (MFA), are not in place.

Workers’ Compensation

Workers’ compensation premium may be affected as healthcare systems increase salaries to retain employees; however, to date we are continuing to see relatively flat renewal rates and even small decreases on good risks.

Management Liability

- Fiduciary Liability

Carriers continue to review and increase mass class retentions, due to ongoing excessive fee concerns. - Directors & Officers and Employment Practices Liability

Rate increases are tapering off, however there is still an emphasis on financial solvency and carriers will thoroughly review financials and ask more questions. Some healthcare segments continue to see reductions in sublimits (i.e., regulatory/antitrust) and increased retentions.

Managed Care Errors & Omissions

Still a limited market with some underwriters reevaluating their book and others showing increased interest in small, regional health plans. Carriers continue to limit capacity and apply higher retentions, lower sublimits and coinsurance.

Recommendations

Despite the ongoing challenges, medical professionals and healthcare organizations facing rate increases can take measures to minimize the impact. Maintaining vigilance and staying up to date on developing legislation can help to anticipate and address changes:

- Partner with a healthcare specialty broker who has access to the largest array of carriers, knowledge of where risks should be placed, and the ability to assist with the quoting process to ensure placement with the appropriate carrier.

- Start the renewal process early and ensure clear communication and transparency. Any changes in operations, including named insureds, should be discussed with underwriters. Clients should also provide details on past financial performance and anticipated changes for the upcoming policy term.

- Secure coverage with an AM Best A-Rated carrier. Longevity and financial stability are very important, and these carriers typically have the highest level of service and reliability, making them better to work with while handling claims and navigating other challenges. They also offer added benefits and resources to help mitigate the risk of claims, keeping premiums low.

- Explore a captive or expand the use of an existing captive. The insurance market has hardened in recent years, and captives are often used for risks where traditional carriers are unwilling to cover or for coverage that is cost prohibitive in the commercial marketplace.

- Evaluate additional risks including billing errors and omissions, active shooter threats, wage and hour, and sexual abuse.

Managed Care, Accident, and Health Reinsurance

Industry Insights

As noted above, healthcare organizations faced a multitude of challenges in 2022. Many of those will continue in 2023. Mergers and acquisitions continue at a rapid pace in both the health plan and the healthcare provider space and C-suite turnover is unprecedented.

As noted above, healthcare organizations faced a multitude of challenges in 2022. Many of those will continue in 2023. Mergers and acquisitions continue at a rapid pace in both the health plan and the healthcare provider space and C-suite turnover is unprecedented.

Suboptimal financial performance by several newer rapidly growing plans has created publicity challenges for the industry and the media has not been kind to “insurtechs” in this space. Reinsurers are extremely cautious as a result. Additionally, the population shift towards more government business continues. This places a significant financial burden on the federal and state governments thereby forcing innovation in both cost and care delivery.

Although the managed care, accident, and health reinsurance space has seen no major entrants or exits this year, navigating these underwriters will require attention and care. Many players in this space have experienced suboptimal results and continue to hone their appetites in response. Along with things like COVID-19 uncertainty and increased claims, poor performance and instability from ACA businesses has impacted this area.

In some cases, underwriter appetites are extremely limited, and the burden is on the client to prove they are a quality risk. This is particularly true for quota share reinsurance, including both traditional and structured quota share programs. At the same time, many buyers who may have viewed reinsurance as a commodity in the past now see the value in establishing longer term relationships with their reinsurance partners, especially those who can reduce losses through a variety of cost containment solutions. Many reinsurers are enhancing their offerings relative to cost containment as a way to differentiate themselves.

Coverage Considerations

Managed care, accident, and health reinsurance markets are proceeding with caution. In the excess of loss space, both the frequency and severity of large claims continue to increase while new risk opportunities such as ACOs are flooding reinsurer capacity.

High-cost specialty drugs continue to increase in numbers and are now joined by a new class of emerging treatments called cell and gene therapies (collectively referred to as CGT). While these therapies are clinically remarkable, they come at a very high cost with most new therapies expected to exceed the $2 million threshold.

In addition to these already approved therapies, the approval of many additional therapies is expected in the coming years. These new therapies’ costs do not have historical experience data, causing underwriters to rely more heavily on conservative actuarial models. All of this has translated into significant variation in terms, conditions, and pricing between markets and intensive disclosure processes. In addition, reinsurers in the quota share space have seen their results negatively impacted by the federal risk adjustment program. This has translated to a higher level of scrutiny on transactions of this nature.

Recommendations

Despite a challenging environment, there are several things that healthcare organizations can do to improve their experience.

- Engage an experienced broker as your strategic partner. Choosing a broker that is well versed in all aspects of healthcare risk financing is critical. Your broker should have strong analytical capabilities

- Build a positive reputation with carriers and reinsurers. Use them as a resource when strategizing about your organization’s progression towards value based care.

- Invest in data. Many healthcare organizations do not have consistent access to timely and accurate data. Making an investment in this process will not only improve outcomes related to insurance and reinsurance placements but will allow for more informed decision making across the organization.

- Consider a wide range of cost containment solutions. Whether directly or through reinsurance partners, solutions to consider include bill audits, out-of-network strategy, large case management, and PBM audits.

- It may also be important to consider exposure relative to emerging therapies and treatments well in advance, so reinsurance options and pricing can be determined efficiently.

Industry Insights

Many marine segments have experienced a boom driven by the influx of boat purchases during the COVID-19 pandemic.

Many marine segments have experienced a boom driven by the influx of boat purchases during the COVID-19 pandemic.

This caused inventory/capacity issues throughout the supply chain. Solid demand continues as buyers seek boats with more power and luxury options, better safety features, and improved energy and fuel efficiencies.

In 2023, we anticipate the used boat market to start to rebound — a significant change, since quality used boats were scarce during the new boat supply challenges. We are finally starting to see an equilibrium between demand and supply.

Newer boaters and first-time buyers continue to drive industry growth. The increase in first-time owners and boaters stepping up to larger, technically advanced yachts is also resulting in more boating accidents, complex claims, and a challenging liability market.

The marine industry continues to consolidate. Family-owned marine operations, marinas, and manufacturers are rolling into large corporations, increasing costs for storage, rentals, maintenance, and repairs. The total cost of boat ownership has increased significantly in recent years and will remain high for the foreseeable future.

Coverage Considerations

Yachting & Recreational Boating

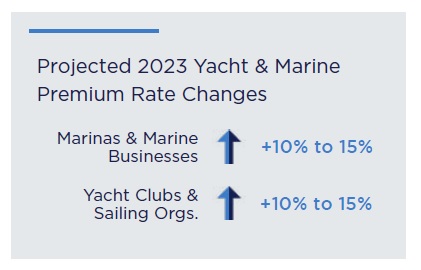

The recreational marine and yacht insurance market remains hard.

The recreational marine and yacht insurance market remains hard.

- In the wake of Hurricane Ian and other storms, the Southeast will continue to experience rate increases and capacity challenges. Coverage for yachts in the Caribbean and International waters will continue to be difficult to place.

- Worldwide cruisers, performance speedboats, wooden yachts, ocean racing sailboats, and yachts older than 15 years are likely to have the most challenges obtaining comprehensive coverage solutions.

- Yachts susceptible to theft and those with complex electronic equipment, quad or more engines, and lithium batteries continue to face strict underwriting guidelines or are being non-renewed.

- High-tech racing sailboats face coverage availability challenges. Repairs are complex and costly. Most carriers do not have an appetite for these risks.

Significant rating factors in the large and luxury yacht markets will continue to be based on vessel technology features, advanced construction, private pleasure usage vs. chartering, experience of the captain and crew, use of a reputable professional management company, and the yacht owner’s and sailing organization’s annual navigation plan.

Marine Businesses

The marine insurance market is seeing tighter reinsurance conditions for coastal property and wind exposures. In addition to catastrophe (CAT) claims, marine businesses, including sailing organizations, are facing a rise in liability claims, driven by a litigious society and social inflation. The maritime community is also experiencing losses arising out of cyberattacks, workplace injury, as well as from allegations of abuse.

Insurers are responding to these unfavorable loss trends and data from catastrophe modeling with increased rates, reduced capacity, and restricted terms and conditions across many coverage lines.

Limit restrictions and decreased capacity for excess liability and directors & officers liability are driving placement challenges and price increases for many marine risks.

Underwriting guideline changes have resulted in reduced appetite for insuring boat builders with less than five years of documented experience. Builder’s Risk policies for vessels under construction highlight the property and marine capacity shortages. Marine business owners should plan for longer lead times and higher premiums, particularly when looking to secure higher-limit policies.

In 2023, the overall marine marketplace is likely to remain hard with fewer insurers participating in the market and more restrictive underwriting guidelines for most business classes. However, we may see some rate moderation for select marine businesses, especially those without coastal exposures.

Recommendations

Begin the insurance process early to have adequate time to successfully navigate the dynamic marine insurance marketplace.

Yacht Owners

- Work with a specialty, consultative insurance broker who understands the complex risks and unique coverage needs that come with yacht ownership and nautical lifestyles.

- Consider including your full personal insurance portfolio (homes, autos, valuables) as part of the marine insurance submission. This not only helps to secure comprehensive coverage that protects all assets and interests, but it can also result in a better, broader yacht policy.

Marine Business Owners

- Work with an experienced marine broker who can create a custom insurance and risk management program through analysis of the existing insurance program, review of exposures and risk factors, and identification of current and future coverage needs.

- Look for insurer stability. Many insurers have tried and failed to penetrate the marine market. Align with a carrier with a long-term commitment to the marine industry.

- Dedicate time and resources to develop and implement risk control programs and loss prevention plans. This is critical to mitigate risks and reduce claims, and can contribute to potential premium considerations on the carrier side. Examples include workplace safety and education programs, expanded alarm systems, and detailed storm preparedness plans.

Industry Insights

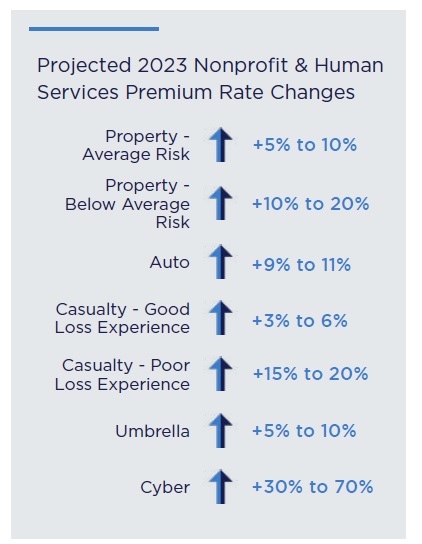

Tight budgets, demands on HR staff resources, managing cyberattacks, and recruiting and retaining employees continue to be major challenges for nonprofits and human services.

Tight budgets, demands on HR staff resources, managing cyberattacks, and recruiting and retaining employees continue to be major challenges for nonprofits and human services.

- Staff hiring and retention is a challenge, with employee benefits a bright spot to keeping staff. Nonprofits are seeing an average 30-35% staff turnover. The continued dependence on federal and state funding affects the sector’s ability to provide needed pay increases. Signing bonuses are not mitigating turnover issues, as many employees will move on to another company for a new signing bonus.

Nonprofits are finding hiring and retention success by implementing better employee benefits outside self-insurance through HRA funding with high deductible plan structure and providing ancillary and voluntary benefits like pet insurance. - Funding and memberships are down. COVID-19 negatively affected many agencies. Even with continued funding, many programs are still not at capacity and many youth services lost memberships, hitting cash flow directly.

- Property premiums for nonprofits and human Services organizations continue to rise. 2022 saw $100 billion in CAT property losses which have directly affected pricing for the entire market, not just those in CAT-prone geographies. This affects Nonprofit and Human Services even if they are outside these traditional geographical situations which experience extreme weather events, such as hurricanes and tornadoes.

- Automobile insurance premiums continue to rise as limited resources and inexperienced drivers have led to more accidents. Driver employee standards have lessened, and driver training programs must be re-established. Limited resources combined with an inexperienced labor pool have added to increased accidents. Rising medical and body shop costs have contributed to increased rates as well.

- Cyber rates are impacted significantly by overall industry loss experience, resulting in greater underwriting scrutiny. More Nonprofit and Human Services organizations are being targeted for ransomware, with payouts and costs associated rising to mid-six figures. Budgetary restrictions make it necessary for nonprofits to utilize outside vendors to provide security and cyber awareness training. This has brought more attention from bad actors to the space in the last five years.

- Employment practice liability (EPL) claims continue to be a source of concern. The fear of social inflation and its impact on Nonprofits and Human Services coverage has resulted in rate increases and higher retentions, to as much as $100,000 per claim. EPL claims have generally arisen from discrimination, wrongful termination, and whistleblowing. Social inflation has resulted in higher claim settlements and nuclear verdicts. Capacity is also limited with many carriers only willing to offer limits of $5 million.

- General liability coverage remains available though abuse coverage is somewhat more challenged. Overall, general liability coverage and limits remain stable and for the most part rate increases are modest. Abuse coverage limits are available from most major providers as a separate limit under the general liability form.

However, many carriers continue to offer minimal limits under the umbrella, generally $2 million for most mid-sized agencies. Concern over social inflation is again the reason.

There does appear to be a willingness from underwriters to consider higher limits but greater scrutiny of agency policy, procedures, training is now preformed.

Recommendations

- Clients should make every effort to invest in risk management and review past loss experience to identify trends. Additionally, they should continue to monitor current loss activity quarterly, at a minimum.

- Establishing internal risk management committees, led by senior management to establish safety recommendations and policy changes when appropriate, is essential.

- Employ root cause analysis to regularly perform claim investigations to identify the real cause of loss, assign accountability to avoid future claims, and implement a solution in a specific timeframe. Once identified, eliminate the cause in a reasonable timeframe.

- Talk to your broker often and early about what is trending with similar accounts to know what to expect in renewals. Ensure that the broker understands the carrier’s needs associated with the industry’s issues, exposures, and solutions.

Industry Insights

The private equity market entered 2023 with depressed M&A activity, the potential for SPAC litigation, and accelerating ESG compliance challenges.

The private equity market entered 2023 with depressed M&A activity, the potential for SPAC litigation, and accelerating ESG compliance challenges.

Dampened M&A activity

- Macroeconomic concerns from rising interest rates, economic inflation, supply chain disruption, labor shortages, and the war in Ukraine will negatively impact companies’ operations, financial results, and share prices and invite shareholder-driven litigation.

- Lower profitability and rising debt costs could lead to employee layoffs, reduction in capital expenditures, and less M&A activity. These challenges may stress private equity portfolio companies’ debt loads, requiring refinancing or additional capital from their sponsor. Underwriters continue to review corporate financials under strict criteria, specifically debt obligations.

Claims against SPACs changing shape

We saw a decrease in SPAC-related securities suit filings in the latter half of 2022. Given the SEC’s heightened focus on these risks, SPACs are no longer attracting the high valuations that caused many of these companies to experience large drops in share price and engender the attention of short sellers. Despite the decrease in SPAC litigation, it is uncertain how this space will develop this year:

- There are still SPACs searching for targets (374 as of January 13, 2023 per Spacinsider.com). The economic environment may pressure SPACs to consummate an unattractive deal or liquidate. In December, 85 SPACs liquidated and returned their investment capital to shareholders. With SPACs liquidating and buying their shares back from investors, the risk of shareholders bringing breach of fiduciary suits seems negligible. That said, we anticipate litigation stemming from regulators and investors pertaining to due diligence, abandoned potential deals, and how liquidation proceeds were distributed.

Environmental, Social and Governance (ESG) raises thorny issues

The SEC continues to be active with its highest level of recoveries. With support from the Biden administration, the SEC is seeking individual accountability to deter future misconduct. In the first eight months of 2022, the SEC proposed 26 disclosures for climate change, cyber, and SPAC structure and governance.

D&O underwriters face challenges as there is not a clear ESG definition or objective way to measure whether a company is a strong ESG risk. Reviewing ESG ratings is not necessarily an indicator of a company’s exposure and carriers use different criteria when analyzing ESG risk.

Coverage Considerations

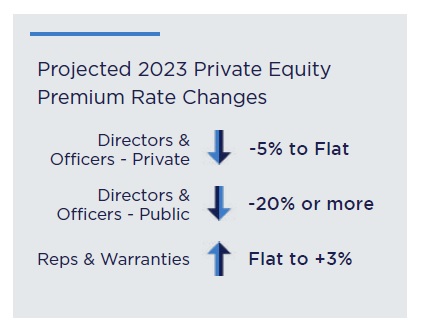

- The representations & warranties (R&W) market has been a roller coaster ride. By the end of 2021, the premium rate hit its high and capacity was limited amidst heavy M&A activity. Fast forward to 2023, and rates have come down substantially due to more R&W capacity as well as the underwriting teams expanding headcount. Now, rates are under 3% for some risks. Additionally, carriers have become more aggressive in areas that underwriters avoided at the end of 2021 and early 2022 (i.e., healthcare).

- D&O has softened from capacity influx, a promising securities litigation environment, and clearer understanding of the pandemic’s economic impact. Companies who may have been forced to structure programs in layers of $2.5 million or $5 million during the hard market are renewing with a $5 million or $10 million limit.

- D&O for public companies continues to soften with significant capacity creating increased competition. Mature public companies are experiencing on average -20% premium decreases and companies that went public in the last two to three years are experiencing on average -30% to -40% decreases. Excess rates continue to come down which has created immense savings opportunities.

- D&O for private companies has also softened, with rates flat to -5% decreases. There is increased carrier interest in writing portfolio programs for PE/VC firms as a way to aggregate their D&O insurance across their portfolio of companies with consistent terms and conditions.

- General partnership liability for private equity and venture funds has softened with average flat to -5% decreases driven by additional entrants to the market and lower excess rates with exception of cannabis and crypto related funds which remain challenging.

- The cyber liability market has stabilized since last year. Improved IT controls are yielding more attractive risks and increasing competition. Companies with strong internal controls are experiencing on average 5-10% increases and companies lacking strong internal controls such as MFA or EDR are experiencing on average 30-40% increase with sub-limits or restricted coverage.

Recommendations

- Meet with your broker at least 90 days in advance of renewal. Specify any changes in the organization, including structure and strategy, or new contractual insurance obligations. Highlight possible involvement with SPACs, crypto, or cannabis. Your broker will work with you to identify insurers that have changed appetite, explain additional coverages available in the marketplace, and establish a renewal strategy.

- Check with in-house counsel, risk manager, CEO, and anyone else who may receive notice of claims, demands, litigation, etc., to ensure that all claims have been reported. Talk to your broker about any circumstances that might develop into a claim.

- Discuss your preferred law firms/vendors for cyber claims (i.e., breach counsel, forensics, etc.), and ensure the firms are pre-approved to avoid potential coverage limitations in the event of a claim.

- For cyber renewals, address any material deficiencies in IT controls in advance to ensure companies are approaching markets with optimal controls.

Industry Insights

The professional services industry, specifically architects & engineers (A&E) and law firms, will see a softer market overall in 2023, with new lines, increased competition, and eased cyber coverage access. That said, the economic downturn and talent shortages will have an impact.

The professional services industry, specifically architects & engineers (A&E) and law firms, will see a softer market overall in 2023, with new lines, increased competition, and eased cyber coverage access. That said, the economic downturn and talent shortages will have an impact.

These are the biggest trends we see in professional services:

- Economic downturns historically lead to increases in professional liability claims, and we expect 2023 to follow this trend. Social inflation, staffing difficulties, and return-to-office challenges keep insurers on edge.

- The cyber market has calmed considerably. While professional services remains a target market for bad actors, many firms have put in risk management controls to garner the best rates.

- Employment practices liability (EPL) insurance took a hit from COVID-19 as predicted. Fisher & Phillips tracked 6,500 cases filed since early 2020, with employment discrimination being the most common type, and healthcare the most common industry.

- New insurers writing specialty lines has created competition. Models, appetites, and budgets may differ, but even the potential for competition is a positive for clients.

- Competition for talent continues to be challenging with fewer graduates, an aging Baby Boom population, and a continuation of the “Great Resignation” prompted by the pandemic. Even with more than 500,000 jobs added in January, firms continue to cite attracting and retaining talent as a primary challenge.

Coverage Considerations

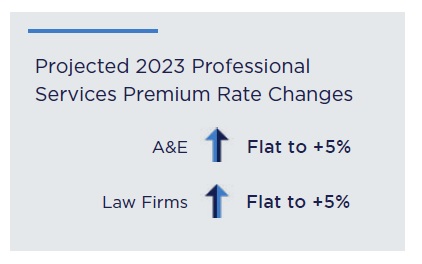

Architects & Engineers

Architects & engineers are deemed preferred risks by property and casualty insurers, as they have less General Liability exposure compared to other industries. Although some of the relatively few players in the P&C space for design firms are seeking rate increases, some healthy competition remains. While some carriers are still attempting to get rate increases that range from the low single digits to as much as 20%, competition has allowed firms with favorable loss histories to find a new insurer (or insurers) to offer terms at or very close to the expiring rate. For the many firms that are experiencing significant growth, rate decreases are not out of the question, as insurers are collecting higher premiums due to the increased exposure basis.

Architects & engineers are deemed preferred risks by property and casualty insurers, as they have less General Liability exposure compared to other industries. Although some of the relatively few players in the P&C space for design firms are seeking rate increases, some healthy competition remains. While some carriers are still attempting to get rate increases that range from the low single digits to as much as 20%, competition has allowed firms with favorable loss histories to find a new insurer (or insurers) to offer terms at or very close to the expiring rate. For the many firms that are experiencing significant growth, rate decreases are not out of the question, as insurers are collecting higher premiums due to the increased exposure basis.

The cyber market has calmed considerably, with firms seeing relatively flat renewals after having seen significant increases over the last two years. As with professional liability, firms that can demonstrate sound risk protocols and that are willing to market their coverage might even expect to see slight rate decreases as compared to what they paid in 2022. Capacity, however, remains tight, with few insurers willing to put up high limits. Where firms are required by key clients to provide limits above $5 million, the excess layers are often priced nearly as high as the primary.

Law Firms

Lawyers’ professional liability (LPL) primary layer insurance rates are now easing. While excess insurers continue to focus on the rate per underlying or the Increased Limit Factor (ILF), additional capacity is leading to competition. ILFs of 30% or lower may be in the past, but an ILF of 40% rather than 50% is more common. Insurers remain focused on the limit of liability offered, and few domestic insurers are prepared to offer more than $5 million.

EPL insurers have pushed for single-digit rate increases for combined management liability and EPL placements for larger firms. Smaller and mid-sized firms with clean loss history can expect flat premium renewals.

Cyber renewals are showing signs of reduced rate pressure. Several insurers reevaluated their underwriting models in the late third and fourth quarters and reduced pricing targets, resulting in relatively flat renewals for firms with excellent controls. For risks that meet the specific underwriting criteria of an MGU, their 2023 renewals may be pleasantly surprising. While not an option for larger firms, smaller firms with good risk management controls may see renewals close to flat. Larger firms typically fall outside of MGU underwriting guidelines and must insure their cyber coverage with the standard market.

Recommendations

Architects & Engineers

- Firms that clearly articulate their approach to risk mitigation on issues such as client-intake and contract review protocols, QA/QC policies, and project closeout policies will differentiate themselves with underwriters and receive optimal terms.

- In the event of a firm’s loss history including paid or open claims, it is important to provide a narrative for each that may include the considerations that went into a settlement and any lessons learned or policies that may have been implemented as a result of the claim(s) to try to prevent future occurrences.

- Cyber risk mitigation remains critical to securing favorable cyber coverage. Clients with better controls, policies, and procedures will receive preferred rates, and those without may be declined.

Law Firms

- With a possible recession, firms should be prepared to discuss financial stability and willingness to alter practice area focus during renewal meetings. M&A value decreased by 38% in the fourth quarter of 2022, and the shift from high-value corporate and transactional practices (capital markets, M&A, and private equity) to counter cyclical practice areas (IP, restructuring, bankruptcy) will be crucial to maintain profitability. The impact of inflation on billing rates and compensation and client acceptance or pushback should be highlighted.

- Return to work, health and wellness, firm culture and collegiality, and attorney training and development remain as issues born in the pandemic. Insurers will be looking at the firm’s flexibility and attention to these issues as part of their overall analysis of a firm’s continued success and risk management culture. Addressing these items in the renewal submission will help the renewal process.

Industry Insights

As a professional buying, selling, leasing, or managing commercial real estate, community associations, retail, hospitality, or habitational, there are a multitude of factors influencing the industry and the risks you face.

As a professional buying, selling, leasing, or managing commercial real estate, community associations, retail, hospitality, or habitational, there are a multitude of factors influencing the industry and the risks you face.

According to The Counselors of Real Estate (CRE), the major issues having significant impact on all sectors of real estate include:

- Mixed macroeconomic conditions

- Geopolitical risks with political, capital markets and real estate market uncertainty

- Societal shifts with the “great decentralization” and trends reversing the flow of people to large urban centers

- Supply Chain disruptions

- Energy sustainability and affordability

- Labor shortages

- Housing imbalances and shortages

- Regulatory uncertainty and growing regulations

- Cybersecurity interruptions

- Growing ESG requirements

Coverage Considerations

All of these uncertainties and evolving issues are having a profound impact on the real estate insurance market.

All of these uncertainties and evolving issues are having a profound impact on the real estate insurance market.

- Inflation and interest rate hikes have greatly increased the cost of construction materials and general pricing. Developers, owners, and tenants are exploring opportunities to lock in material prices, negotiate lease terms, and amend contracts to manage costs, as well as evaluating and selecting profitable properties in desirable markets.

- Extreme weather events like hurricanes, floods, and wildfires are raising premium prices for both clients in affected areas and as a whole. The impact of climate change on real estate is raising concerns among experts due to the risks it poses to property and communities. The threat of climate change risks, natural disasters, and environmental changes is shifting everyone’s perspectives on where and how to invest in property.

Net result: the insurance market for real estate continues to be in a state of transition and uncertainty. All but the best and most favorable risks will likely face increasing premiums and deductibles, reduced limits, and potentially declining coverage in CAT zones or areas of increased risk of weather events.

Businesses with prior losses and catastrophe exposures may experience the most significant challenges, with limited options, capacity tightening and rising premium costs. See our Risk Management section for additional detail on practical steps you can take to positively influence your outcome.

Recommendations

Given the uncertainties and complexities of the industry, we recommend that you work with a real estate insurance brokerage specialist to understand your risk profile and take steps to ensure that you are adequately protected and have a risk mitigation/management plan in place. Risk control and analytics is particularly important for this segment. Other practical considerations:

- Update property values to avoid penalties on rates or increased premiums. Given rising building costs, it is crucial to proactively obtain updated replacement cost appraisals before renewal to aid in negotiating fair market rates. Submissions containing factually supported up-to-date valuation data will help carriers price coverage accurately and ensure sufficient coverage for property reconstruction or replacement.

- Understand the factors going into rate increases. The rate charged per unit of insurance is increasing due to inflation and growing exposures, while the premium amount — rate multiplied by the number of units purchased — is increasing due to higher insurance-to-values. Understanding the difference can help set appropriate cost and coverage expectations.

- Prearrange with your broker to prepare for policy renewal as soon as possible. Early planning allows time to prepare for potential policy changes. Due to volatile inflation, consider scheduling quarterly broker meetings to adjust coverages for current market conditions.

- Consult with your broker to examine your current coverage terms and conditions, including any exclusions. Confirm that your policy limits and sub-limits are sufficient to cover potential losses. Verify property valuations to ensure accuracy. Confirm coverage for recovery expenses after a loss, considering current repair and rebuilding cost inflation.

Industry Insights

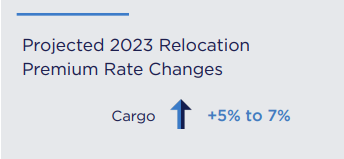

The Relocation and Household Goods (HHG) transportation industry continues to be impacted by the COVID-19 aftermath, the economic downturn, and anticipated impacts of the Department of Defense Global HHG Contract (GHC). These forces have led to consolidation and a shrinking labor pool of experienced moving and driving crews, causing service quality issues and claims increases. While a slowing economy may shift additional labor supply back to moving and storage industry service providers, the overall threat of declining service capacity is likely to continue to negatively impact service quality and loss ratios.

The Relocation and Household Goods (HHG) transportation industry continues to be impacted by the COVID-19 aftermath, the economic downturn, and anticipated impacts of the Department of Defense Global HHG Contract (GHC). These forces have led to consolidation and a shrinking labor pool of experienced moving and driving crews, causing service quality issues and claims increases. While a slowing economy may shift additional labor supply back to moving and storage industry service providers, the overall threat of declining service capacity is likely to continue to negatively impact service quality and loss ratios.

The Federal Court of Claims’ favorable GHC ruling at the end of 2022 allows the winning bidder to start implementing the largest moving contract in the world, valued at $6.2 billion over the first four years. Small and medium movers not part of the winning bidders’ network, many of whom rely on business from the Department of Defense, may be forced to dramatically scale down operations or even shut down altogether. This may result in regional or industry-wide capacity shortages during the May to September peak moving season, exacerbating lingering labor shortages and service quality deterioration.

While there are several factors that have contributed to the overall increase in claim settling costs, inflation is chief among them. The average cost of replacing major household goods has increased by nearly 20%, and as a result, it is estimated that average claim costs will continue to be 9% to 12% higher than pre-pandemic levels.

Recommendations

With the increase in service quality issues and claim costs due to a lack of experienced household goods moving and driving crews, it is recommended that clients:

- Lean on analytics to identify moving supplier performance issues that can be addressed through training or consolidation of suppliers.

- Ensure that coverage limits are reflective of the increased cost of replacing major households to avoid underinsuring shipments in the event of a total loss.

- Review your current policy with a specialist broker to ensure it is broad enough to prevent gaps in coverage, which can lead to contentious claim issues and poor relocation experiences for transferees.

- When evaluating coverage/insurance options be sure to confirm that your policy is financially backed by a highly rated insurer.

Industry Insights

Commercial transportation continues to grow, but the challenges are ongoing.

Commercial transportation continues to grow, but the challenges are ongoing.

There is increased demand for last-mile deliveries due to growing ecommerce popularity and customer buying trends. However, there is a labor shortage, and this has led some businesses to prioritize short-term goals over safety regulations and overall business longevity.

To meet immediate demands, business may put less qualified drivers on the road, adding additional risk and exposure to increased claim severity, nuclear verdicts, increased litigation, and rising medical expenses.

Driver employment classification versus 1099 contractual agreements remains top of mind for businesses. While the contract gig-economy model is an easy way for companies to get drivers behind the wheel while saving on payroll expenses, it creates a revolving door of inexperienced labor that allows industry setbacks to persist. As employee retention is more cost-effective than hiring and training new labor, employment classification will help many businesses save from potential disaster-related costs in the future.

Coverage Considerations

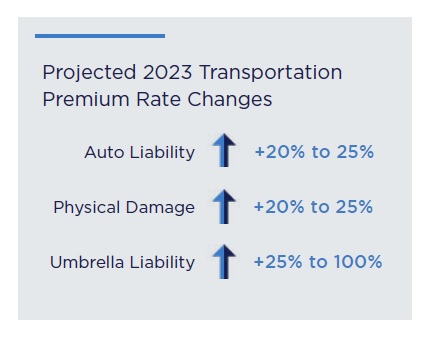

The transportation industry remains a hard market. Specific risk factors continue to fuel the premium increases from last quarter, with physical damage hitting +20% to 25% and umbrella liability +25% to 100%, as well as auto liability rising even further to 20% to 25%.

The transportation industry remains a hard market. Specific risk factors continue to fuel the premium increases from last quarter, with physical damage hitting +20% to 25% and umbrella liability +25% to 100%, as well as auto liability rising even further to 20% to 25%.

Less experienced drivers have contributed to an increase in the frequency and severity of auto liability insurance claims. The severity of auto claims has increased over the last two years from an average of 13k to 38k, all in tandem with social inflation, driving premium and umbrella rates higher.

Physical damage, increased thefts and the rising cost of auto parts are also affecting auto liability and property rates. With rising inflation and the impacts of supply chain challenges of the past year, costs have risen from physical damages to transportation vehicles.

Inherent risks in the industry are also contributing to higher umbrella liability rates. The significant growth of claims and resulting nuclear verdicts are contributing to higher liability coverage rates as insurance carriers deal with the overall risk scenario of the transportation industry.

The industry awaits a significant positive impact once there is widespread implementation of new technologies such as high-end GPS and monitoring software.

Recommendations

- Motor vehicle records (MVRs) are being scrutinized more than ever before by underwriters. It is crucial for businesses to maintain strict safety standards and procedures to minimize potential losses.

- In the event of litigation, companies that continue to hire drivers with a history of infractions or allow service hour violations may be severely impacted. Implementing better hiring practices, in addition to safety technology such as collision avoidance systems, telematics, and cameras, can help protect against future liability issues.

- It is prudent for businesses to ensure Federal Motor Carrier Safety Administration SAFER scores are below the national average. If not, working with a third-party consulting service to reach a better number is imperative.

- While it may be tempting for businesses to reduce coverage in an effort to lower costs, doing so may not provide adequate protection in the face of increasing industry risks. As a result, transportation businesses are exploring alternative coverage options such as captives, risk reduction groups, and higher deductible programs to provide a safety net in the long term.

Industry Insights

The 2023 insurance market for waste & recycling companies will continue to be challenging across most coverage lines due to limited capacity and increased claims frequency and severity. Capacity and claims have been negatively impacted by:

The 2023 insurance market for waste & recycling companies will continue to be challenging across most coverage lines due to limited capacity and increased claims frequency and severity. Capacity and claims have been negatively impacted by:

- Frequency of auto liability and physical damage claims

A nationwide driver shortage, distracted driving, more vehicles back on the roads, and the increased costs to fix vehicles has led to higher claim frequency and costs. - Nuclear verdicts and high jury awards in the transportation industry

Plaintiff’s attorneys continue to focus their attention on trucking companies who they believe may put short-term revenue goals ahead of safety measures such as driver training and safety technology due to driver shortages and cost containment measures. - High workers’ compensation rates

While Workers’ Compensation rates have been coming down in many industries for several years, the Waste & Recycling industry continues to be challenged due to the nature of the work conducted. Occupational Safety and Health Administration (OSHA) ranks the most dangerous work according to fatality rates. In 2022, OSHA ranked Refuse Waste and Recyclable Material Collectors as the sixth most dangerous with a fatal injury rate of 33.1 per 100,000 workers. - Carriers exiting this market

After several years of carriers exiting the property market for waste & recycling facilities, there is still limited insurance and reinsurance capacity due primarily to the fire exposure. Fires at Waste & Recycling facilities are often caused by the improper disposal of lithium batteries. Ryan Fogelman, a partner at Fire Rover, a fire detection and elimination solutions firm, has been tracking fires at waste & recycling facilities since 2016. According to Fogelman, 2022 surpassed 2021 and 2018 as the worst year for waste & recycling facility fires in the U.S. and Canada with 368 fire incidents.

Recommendations

With the challenging marketplace for waste and recycling companies, clients need to make sure that they are being presented in the most favorable light to the insurance marketplace.

We recommend they focus on:

- Strengthening and showcasing their safety initiatives, training programs, fleet improvements, and driver hiring criteria.

- Promoting use of telematics and showing how this information is used for future driver coaching and training.

- Reviewing their SAFER scores and providing a grid to show maintenance and driver safety improvements.

- Assessing their property conditions and making improvements.

- Analyzing the costs and risks of alternative funding options and high deductible programs.