2023 State of the Market - Private Client Services

Industry Insights

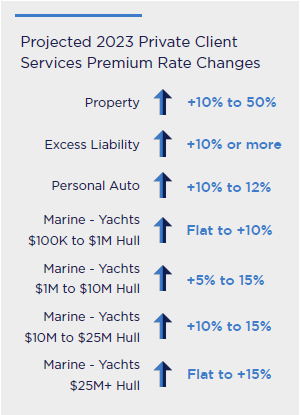

We are seeing the impact of continued turbulence across the personal insurance landscape in 2023, particularly for high net worth (HNW) individuals and families. The role of the independent broker has taken on added importance, as homeowners in traditionally affluent pockets of the U.S. grapple with diminished coverage capacity.

In addition to devastating natural disasters and increased auto loss severity trends, rising costs for marine and yachts, and fine art or other collections, carriers supporting this market segment are making necessary pivots to remain viable.

- The severity and frequency of catastrophic (CAT) events in premium coastal and mountain communities have led to record losses. According to Climate.gov, “the costliest 2022 events were Hurricane Ian ($112.9 billion) and the Western and Central Drought/Heat Wave ($22.1 billion).”

- Reinsurance costs increased by double digits over the past two years and show no signs of abating, which typically means ongoing property insurance rate increases. Compounding matters, property claim costs skyrocketed as well due to inflation and supply chain issues.

- Auto insurers face soaring losses as driving returns to pre-pandemic levels with claims frequency and severity on the rise. Costs to repair or replace vehicles have spiked due to a shortage of parts and new and used cars.

Throughout 2023, we expect a continued hard market environment in Personal Lines across all lines of business. Clients with property in disaster-prone states such as California and Florida will remain challenged as carriers continue to reduce coverage availability. Carriers will be focused on reducing volatility in their portfolios by tightening underwriting guidelines and limiting risk exposure.

Excess & Surplus insurance in high demand to mitigate exposure

Understandably, current market conditions have led to dramatic demand and growth for Excess & Surplus (E&S) insurance. With the flexibility of rate and form afforded in the E&S market, carriers can provide greater solutions for clients in high-risk areas and adapt to change more nimbly.

Personal automobile a difficult market

Rate increases are anticipated in the personal automobile line of business with all carriers. The auto industry is experiencing its worst results in decades. Carriers have not been able to adjust rates or coverages to keep up with inflation and loss trends.

“Nuclear” settlement trends driving up umbrella rates

Driven by social inflation and the increasing cost of litigation, personal liability settlements continue to increase. “Nuclear verdicts” — those over $10 million dollars — are increasingly common. As these trends continue, rates are expected to rise.